iPartners inFocus - Recessions: what do they look like?

In this edition of inFocus, Michael Blythe considers recessions and what they look like. (By Michael Blythe, 9th August 2023)

• Recession fears are elevated. Recessions are painful.

• Having an idea of what triggers recession and what they look like is useful background for households, businesses and policymakers.

• Falling private investment drives the typical recession. Public spending and net exports provide some offset. Consumer spending reacts later as unemployment rises.

• Recessions are typically triggered by an economic or financial shock. Or a policy mistake.

• High-frequency indicators are a useful tool to assess recession risks.

Every turn of the mortgage screws as interest rates rise, every turn of the household budget screws as

prices rise and every warning about economic threats bring with it fears of a recession.

It’s a common human trait to see something going wrong and extrapolate from there to the worst-case

outcome. Every sneeze means Covid. Every negative economic signal means recession.

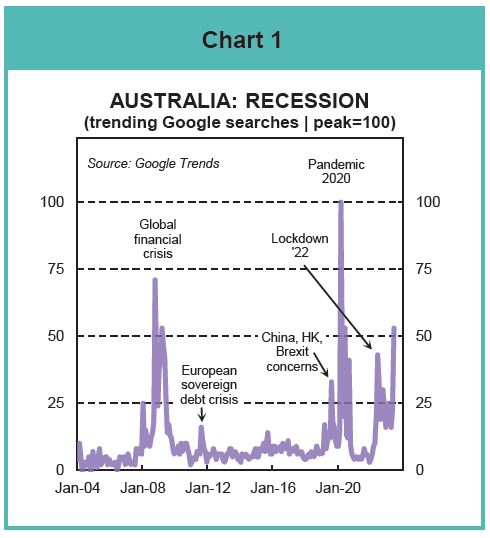

Those worst-case fears are readily revealed in our online search activity. It finds expression in the frequent spikes in searches for “recession” (Chart 1).

One of these “spikes” is underway now. And it is hardly surprising given the frequent warnings from RBA Governor Lowe about the “narrow path” that lies between entrenched inflation and rising unemployment. Treasurer Chalmers comments about “difficult times” and “difficult decisions” adds fuel to the fire.

Recessions are painful. They involve potentially large output losses and rises in unemployment.

Having an idea of what triggers recession and what they look like is useful background for households, business and policy makers. Getting advance warning of impending recession is valuable information for those groups.

This edition of iPartners inFocus looks at these topics, with a particular focus on what the high frequency indicators are telling us about the current state of play.

The message from these high frequency indicators is that recession risks are real. But they have receded recently. Our chief policy makers warn of recession. But their forecasts look more like an extended period of economic weakness and a modest lift in unemployment (Chart 2).

What is a recession?

Surprisingly, there is no agreed definition of “recession”.

The two-negative-quarters-of-GDP-growth definition beloved of newspaper editors is purely arbitrary. And it can mislead at times. So Australia supposedly avoided recession during the Global Financial Crisis (GFC) in 2008-09 because of the random pattern of quarterly GDP growth. But those who experienced first-hand the 2ppt rise in the unemployment rate during the GFC would disagree.

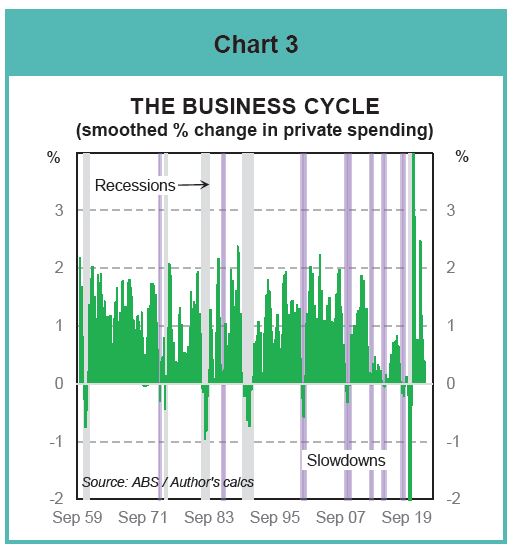

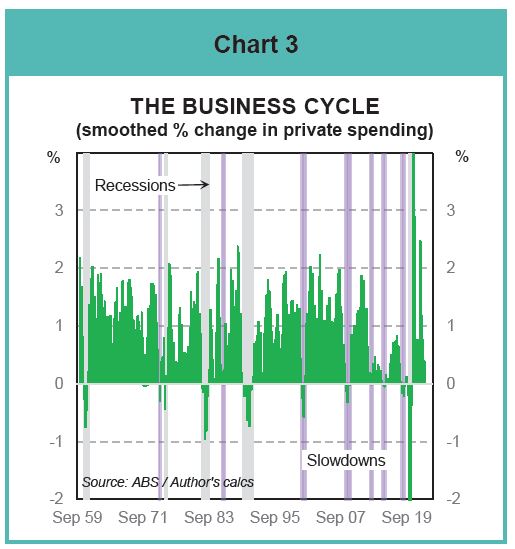

We can probably all agree that a recession is a period of weak economic growth and rising unemployment. But that is still a little vague. And the waters are muddied by the components of GDP behaving differently during a downturn. My preferred indicator of the overall business cycle is private spending.

This measure avoids some of the offsetting tendencies evident in broader indicators of activity that would otherwise cloud the picture. The “automatic stabilisers” in public spending, for example, often moderate the impact of a downturn in GDP growth. And a build-up in inventories and an improvement in net exports often mute the early stages of a downturn.

Outright falls in private spending clearly mark the five major recessions of the early 1960s, the mid 1970s, early 1980s, the early 1990s and 2020 (Chart 3 - grey shaded areas).

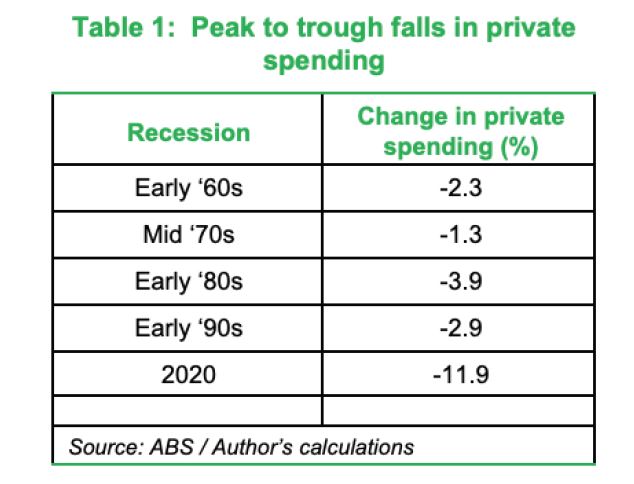

The typical recession involves peak-to-trough falls in private spending of 1-4% (Table 1).

Of course, the idea of a typical recession was blown out of the water by the pandemic-induced recession of 2020 – private spending fell by nearly 12%!

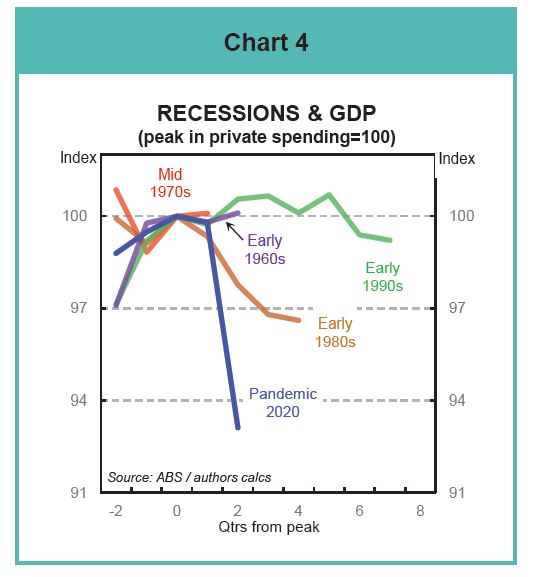

The 2020 recession hides the underlying features of a recession and distorts the analysis (Chart 4). The pandemic recession is excluded in the remaining analysis.

The spending calculations also reveal economic slowdowns that fall short of recession are a regular feature of the economic landscape (Chart 3 - purple shaded areas).

What do recessions look like?

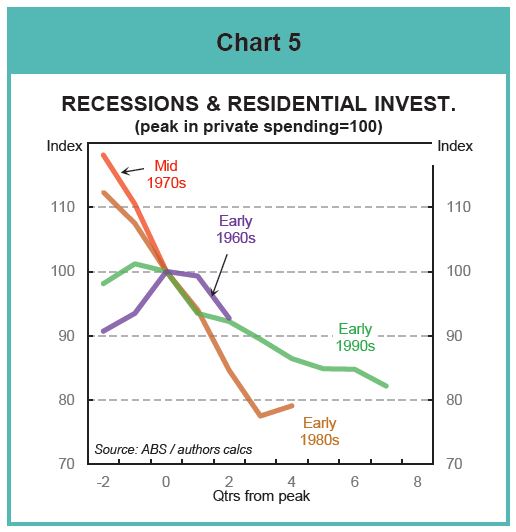

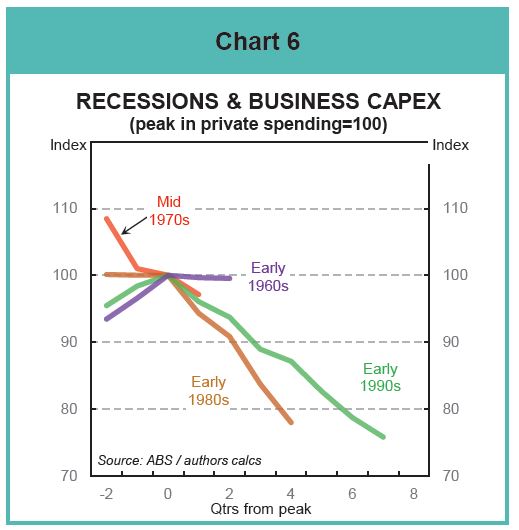

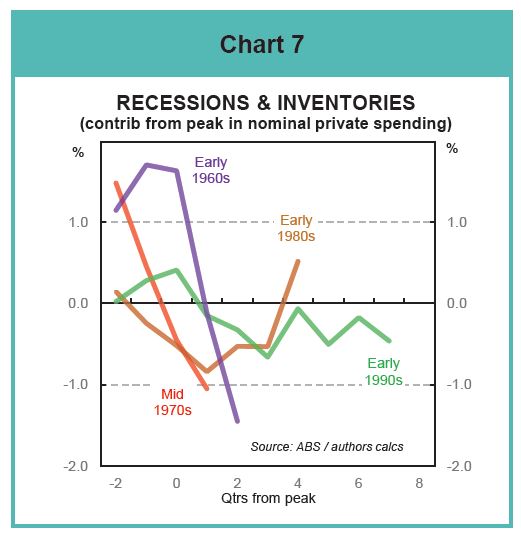

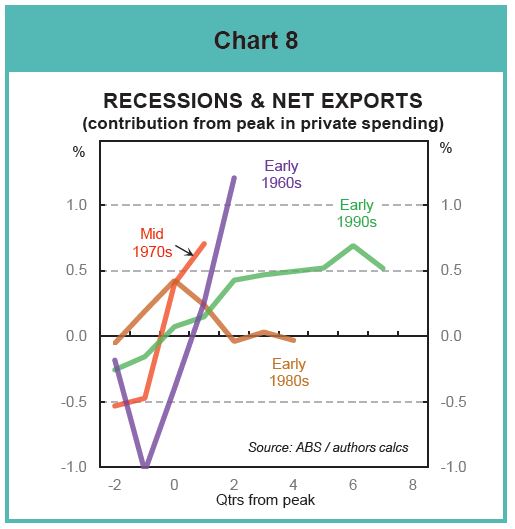

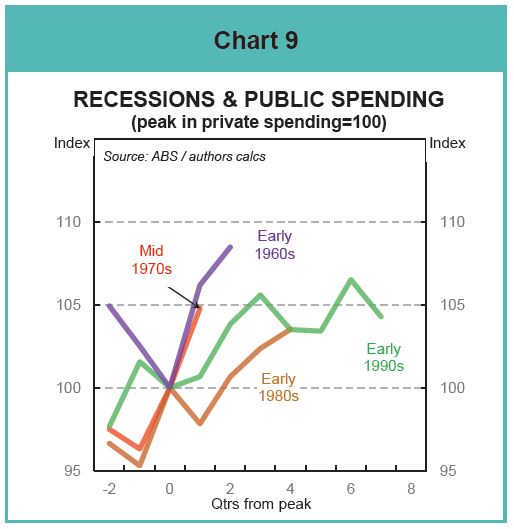

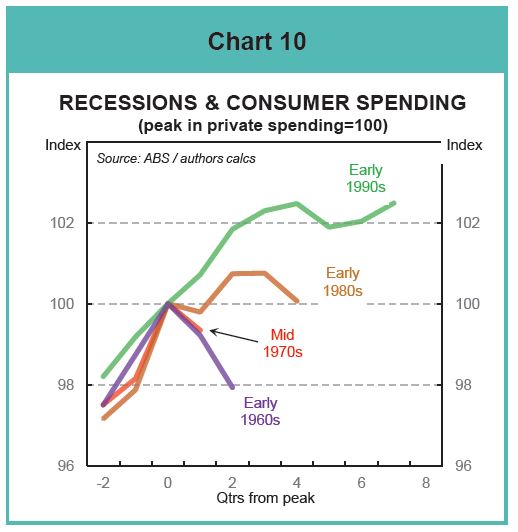

A closer look at the patterns behind previous downturns and slowdowns in the Australian economy reveals a number of common themes. Charts 5-10 show the path mapped out by the major spending aggregates after previous business-cycle peaks:

The typical recession is driven by a sharp downturn in private investment. Dwelling construction falls sharply…

… and business capex is reined in as companies slash capex plans.

An initial (unintended) lift in inventories often supports growth before a (deliberate) inventory unwind occurs…

… and a contribution from the “rest of the world” helps as import growth slows more than exports.

Public spending tends to pick up sharply – part automatic, partly counter-cyclical policy.

Consumer spending shows a late-cycle reaction to recessions as unemployment lifts.

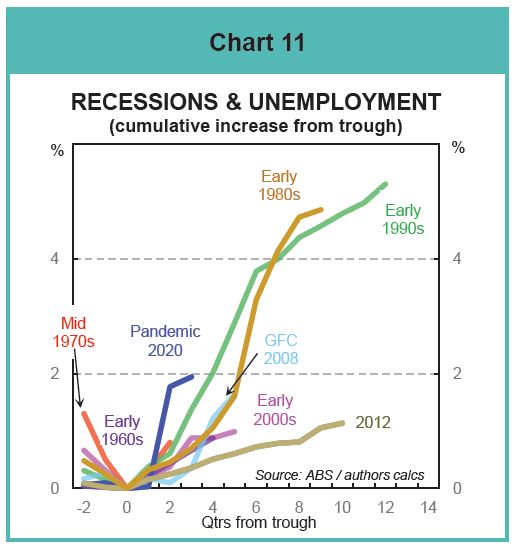

The other common theme in a recession is that unemployment lifts (Chart 11). But the labour market response can vary significantly. There have been two types of labour market shakeout:

• the unemployment rate rises by around 5ppts, effectively doubling (eg 1981, 1989);

• the damage is limited to an increase of 1-2 percentage points (eg 1972, 2000, 2008, 2012, 2019).

One differentiator is the degree of labour market slack. The larger job losses occur when labour market slack is already elevated. The smaller losses occur when labour markets are “tight”. Employers are more inclined to “hoard” labour in those episodes. Today’s labour market is “tight” – favouring only a modest rise in unemployment if recession hits.

Another factor in more recent cycles is a lift in flexibility. Employers have been more inclined to vary conditions (eg hours worked) rather than reaching for the job-cut lever. And employees have been more inclined to accept those variations.

The evidence also shows that a strong policy response can limit the labour market damage. The massive fiscal and monetary stimulus applied during the pandemic is an example.

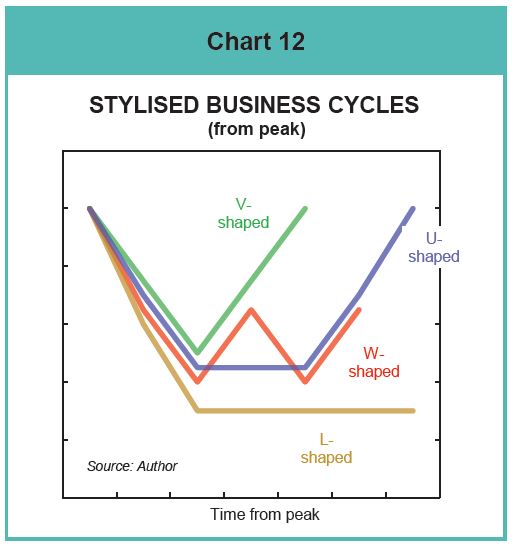

The economist’s rule-of-thumb when thinking about a recession and what it might look like is to pick a letter:

a “V”, “U”, “W” or “L”. In short:

• A V-shaped recession involves a short, sharp shock with the economy recovering quite quickly (Chart 12).

• A U-shaped recession where the economy bounces along the bottom for a while before recovering.

• A W-shaped or “double-dip” recession where there is a false recovery before the economy slides back again.

• An L-shaped recession where the economy struggles for an extended period.

What triggers a recession?

Every recession has its own unique features. But there are some broad categories of recession triggers. These include:

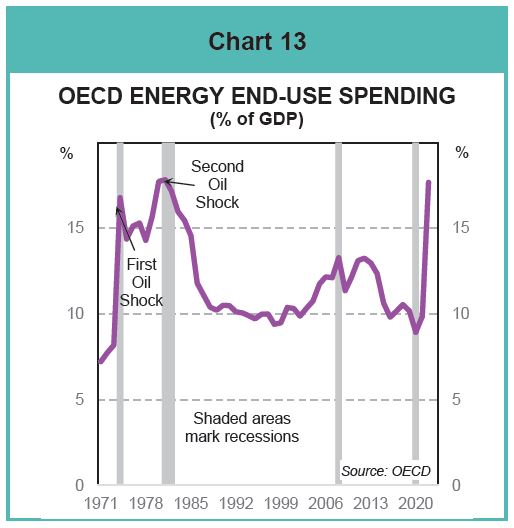

i. An economic “shock”

The classic example is the oil price shock of the mid-1970s (Chart 13). The global oil price quadrupled at the time. The price shock and policy response resulted in recession (and stagflation).

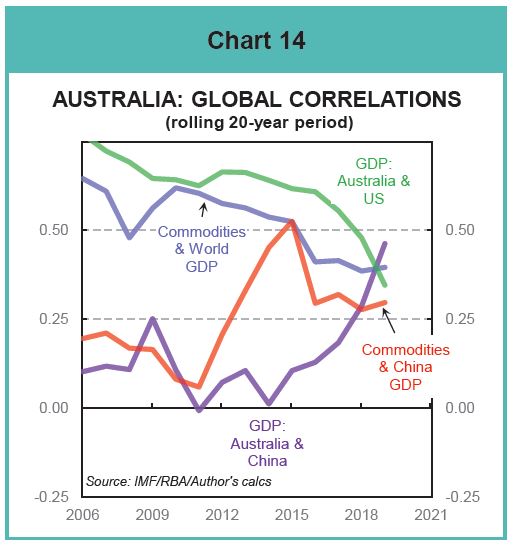

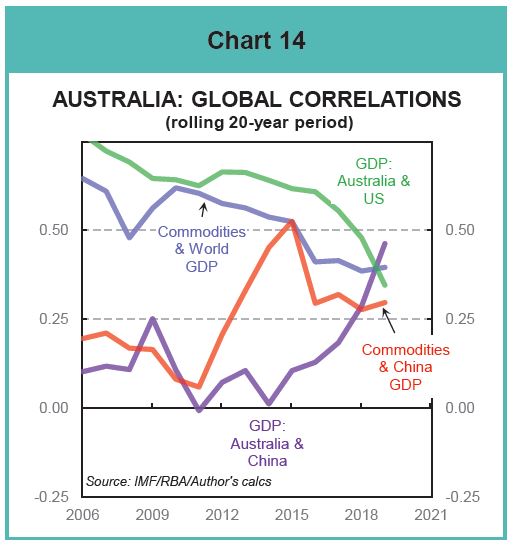

As a small, open economy the shocks that hit Australia often get a “made overseas” tag (Chart 14). So the pandemic and the policy response such as lockdowns and border closures generated a global recession which, even with a massive policy response, Australia could not escape.

ii. A policy “mistake”

Australian policy makers moved decisively in the late 1980s to crush inflation. Interest rates were lifted to historically high levels. And, with all the clarity of 20-20 hindsight, those levels were too high. The policy mistake ended with what Treasurer Keating called at the time “the recession we had to have”.

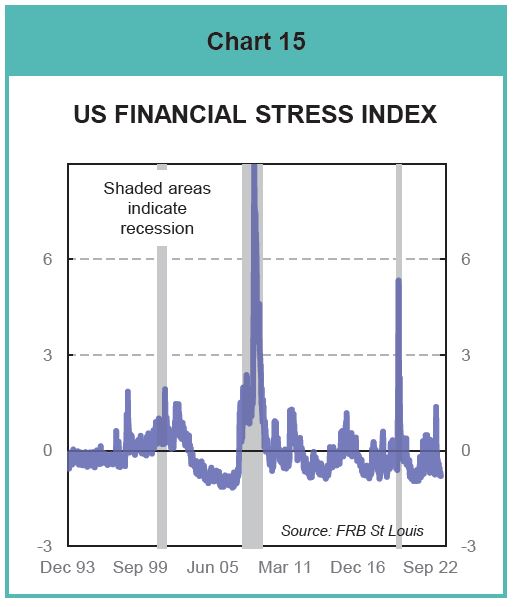

iii. A financial “shock”

The importance and interconnectedness of the global financial system can magnify and transmit financial shocks around the world. The Global Financial Crisis is a case in point (Chart 15). Problems in US housing markets spilled over into financial strains more generally with a knock-on effect to global markets.

Where are we now?

As we sit here in 2023, elements of all these recession triggers are in play.

There is an economic shock courtesy of high and rising prices and their impact on household budgets. An external economic shock threatens as China, the US and Europe flirt with their own recessions.

There is scope for a policy mistake if the RBA pushes through the one-rate-rise-too-many. The rise in mortgage payments and the rollover of fixed rate home loans as they mature bring elements of a financial shock.

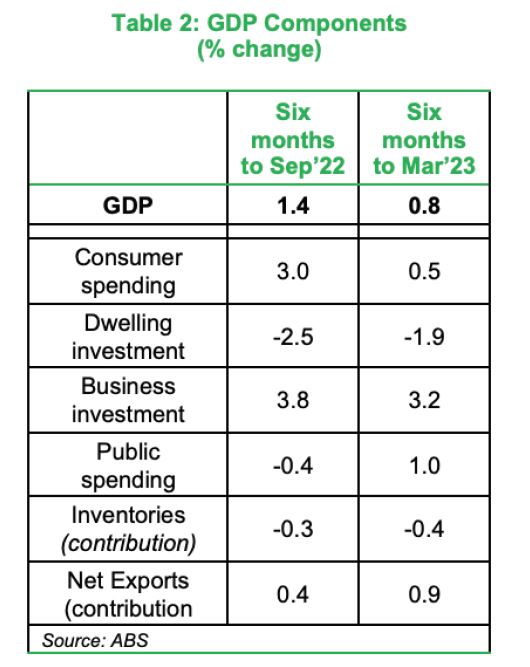

There is also evidence of recession patterns in the economic data (Table 2).

As with the typical recession discussed earlier, a downturn in residential construction is underway. And public spending and net exports have lifted. But business capex remains resilient and there is no evidence of an inventory build-up. The consumer spending picture is mixed. But unemployment remains around 50-year lows.

The bottom line is that the direction of risk is still towards recession. The consumer is the major source of that risk. But the most likely outcome remains a period of sub-trend economic growth.

What are the high frequency indicators telling us about recession risks?

Against this backdrop, a selection of high frequency indicators are important tools in the analyst’s arsenal.

The overall message is that recession risks are real. But they have receded recently.

The global economy is one source of recession risk.

Global growth has slowed. And the main forecasting agencies warn of global recession. The keys for Australia are the US and China. The US is important because of its central role in global financial markets. China is important as Australia’s major trading partner. The importance is illustrated by the high correlation between Australian, American and Chinese GDP growth (Chart 14).

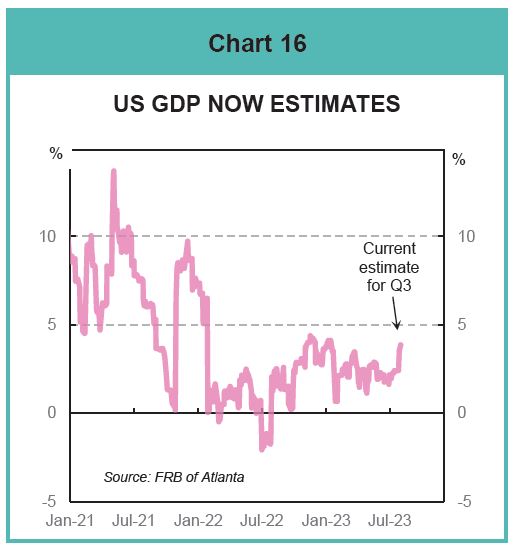

The daily nowcast estimates of GDP growth published by the Fed Reserve Bank of Atlanta show the US economy is, if anything, picking up (Chart 16).

Nowcasting involves combining complex modelling techniques with the latest data readings to estimate GDP growth.

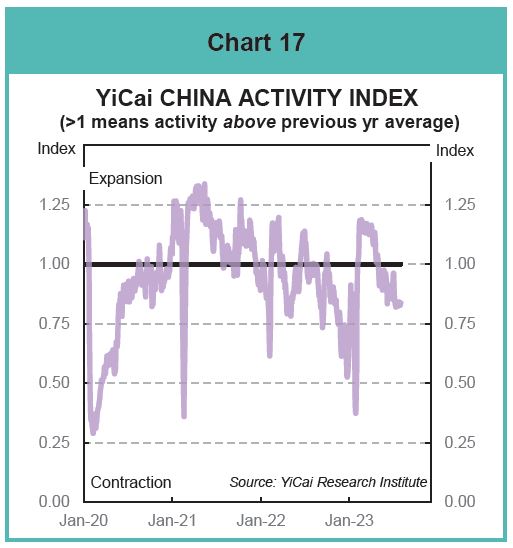

High frequency (daily) indicators for China, however, show some deterioration. Measures of traffic congestion in Beijing and Shanghai, for example, are edging back below 2019 averages (or pre-Covid). The YiCai daily China Activity Index, that combines many high-frequency indicators, is also below “normal” levels (Chart 17).

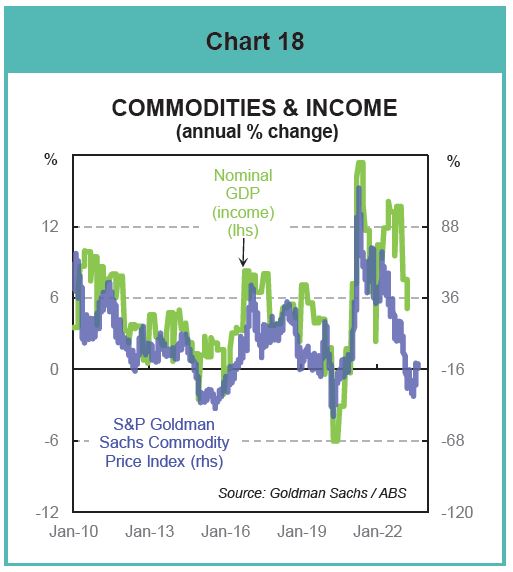

One of the main transmission channels between the global economy and the Australian economy is commodity prices. The swings in commodity prices are a key driver of nominal GDP growth. Nominal GDP is essentially national income – it covers wages, profits, investment incomes and the like.

The S&P Goldman Sachs Commodity Price Index is a high frequency indicator of the general direction of commodity prices. The recent turn in GSCPI growth rates suggests some of the downside risks to Australian income growth are easing back (Chart 18).

The focus on commodity prices provides a reminder that financial markets more generally provide a lot of information on the economy more broadly.

The yield curve, for example, is the sum total of a significant amount of information. The shorter end of the yield curve

reflects current and expected monetary policy settings.

These settings are an important driver of near-term economic activity. The longer end of the curve summarises expectations of future inflation and real interest rates. And so are an indicator of where the market believes the economy is heading from a longer-term perspective.

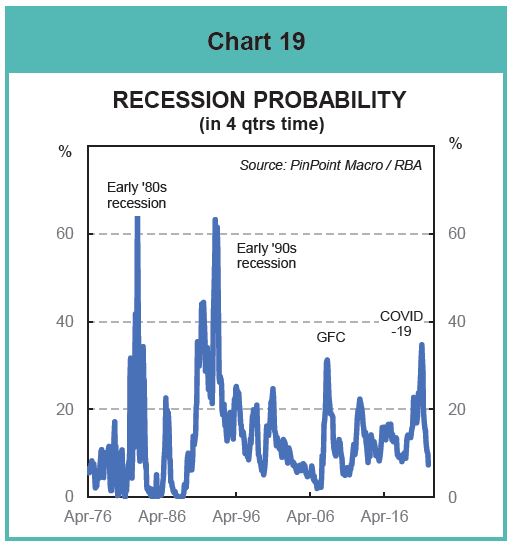

In reality, the slope of the yield curve reveals what markets are pricing in for the risk of recession. The current recession probability is low (Chart 19).

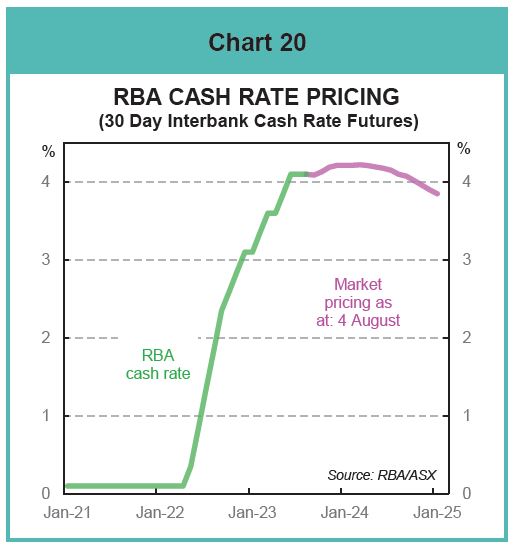

The other financial pricing to follow is where the market thinks the RBA cash rate is heading. The market is pricing the cash rate near a peak. And there is a chance of lower rates in 2024 (Chart 20). The chance of a policy mistake triggering a recession is receding.

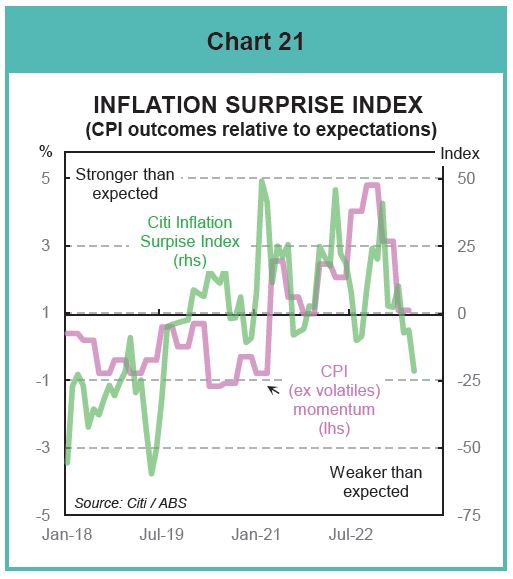

The Citibank Inflation Surprise Index reinforces the current market pricing for peak cash rates / future cuts. The Index measures the gap between actual and expected inflation outcomes. The gap has shifted into negative territory – inflation pressures are now weaker than expected. This shift is typically followed by a slowing in inflation momentum (Chart 21).

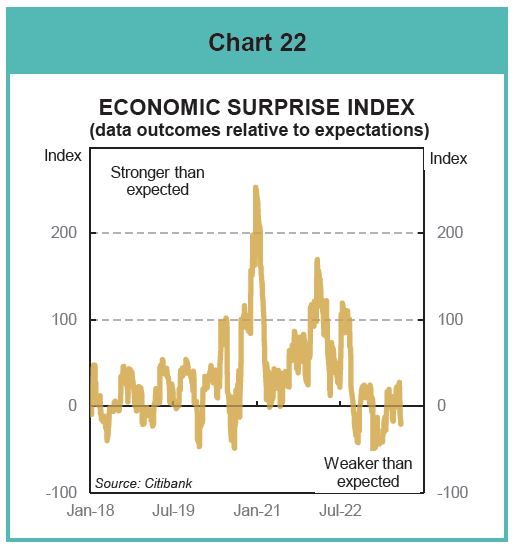

Citibank also construct a daily Economic Surprise Index. The index measures the extent to which key economic data is either beating or missing expectations. A positive surprise means actual data outcomes are better than expected. And vice versa. The Australian Economic Surprise Index has lifted off its recent lows. And it now looks to be stabilising around the neutral zero line (Chart 22). The Index is not showing the ongoing slide that signals recession.

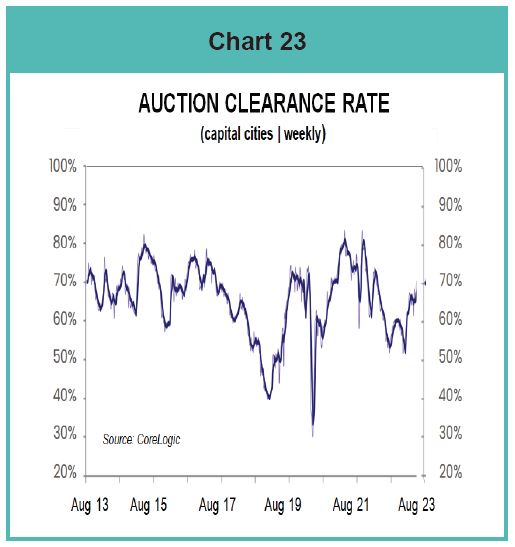

The current downturn in residential construction is consistent with the typical recession pattern. But leading indicators like auction clearance rates are turning up (Chart 23). Dwelling prices and residential construction usually follow. Fundamentally, the rapid acceleration in population growth as migrants and students return means more dwellings are required.

Various editions of iPartners inFocus have consistently identified the consumer as the source of greatest risk facing Australia.

Households have been squeezed by rising prices at a time of sluggish wages growth. Disposable income has been hit by rising mortgage payments and some surprising strength in tax payments. Household wealth has suffered as dwelling prices fell. Savings buffers have eroded.

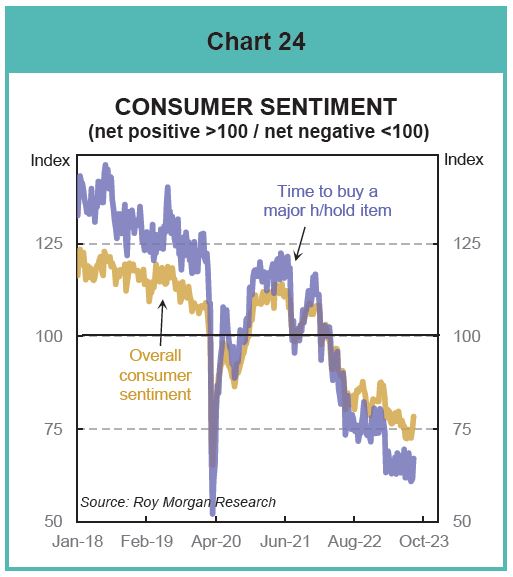

Not surprisingly, weekly reads on consumer sentiment and spending plans have weakened sharply (Chart 24). The deterioration in these measures appears to have ended. But current levels are consistent with a consumer recession.

The official data does show a decline in consumer spending. But more timely indicators show that this slowdown remains relatively muted compared with the typical recession experience.

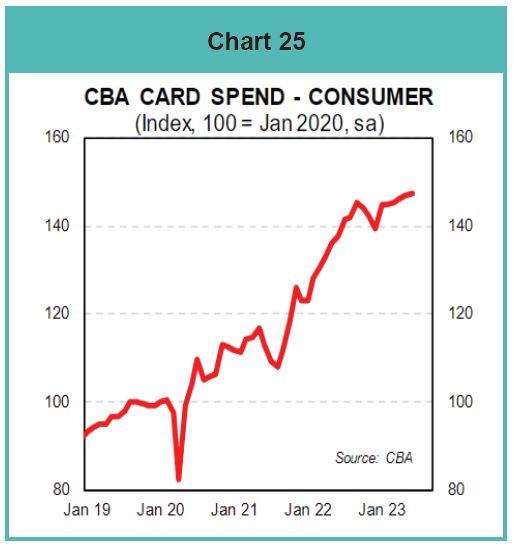

The commercial banks have access to an incredible array of timely information generated by their businesses. CBA’s credit card business, for example, gives a very up to date read on consumer spending trends. The data shows spending growing at a modest pace (Chart 25). The outright falls associated with consumer recessions are not evident.

The labour market is the missing piece of the jigsaw. Ongoing jobs growth has supported spending.

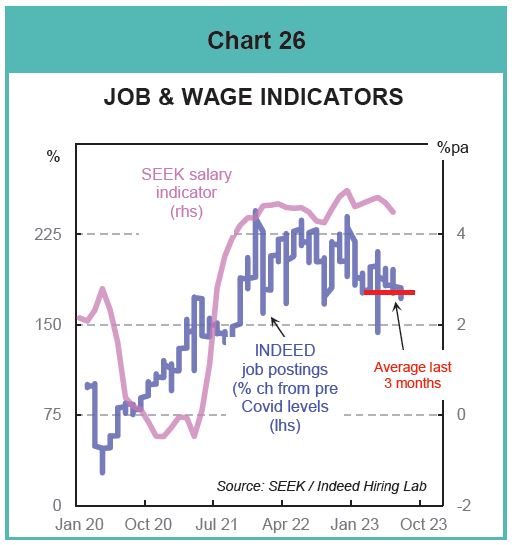

Tends in high frequency data, such as the daily reads on new hiring collected by Indeed Hiring Lab, remain encouraging. New job postings have levelled out in the past few months but there is no indication of layoffs (Chart 26). And labour market “tightness” has, according to the SEEK Salary Indicator, delivered some increase in wages growth (Chart 26).

Looking ahead:

• If wages keep growing at the 4-5%pa pace suggested by the SEEK indicator and inflation slows in line with the Citi Inflation Surprise Index then real wages will rise in 2024. Delivering the Stage 3 tax cuts would help.

• If dwelling prices move in line with CoreLogic auction clearance rates then household wealth will rise.

• If market pricing for the top in the RBA cash rate is correct then the household debt service ratio should peak below the 10% of disposable income figure associated with past consumer recessions.

A lot of ifs and buts. But there is a good chance of avoiding a consumer recession.

Meanwhile, I’m off to give the credit card a workout!

Disclaimer:

This report provides general information and is not intended to be an investment research report. Any views or opinions expressed are solely those of the author. They do not represent financial advice.

This report has been prepared without taking into account your objectives, financial situation, knowledge, experience or needs. It is not to be construed as a solicitation or an offer to buy or sell any securities or financial instruments. Or as a recommendation and/or investment advice. Before acting on the information in this report, you should consider the appropriateness and suitability of the information to your own objectives, financial situation and needs. And, if necessary, seek appropriate professional or financial advice, including tax and legal advice.