iPartners inFocus - Budget ‘22 – Once more to the breech!

iPartners inFocus - Budget ‘22 – Once more to the breech!

Michael Blythe's latest iPartners inFocus looks at the budget which delivered what was promised – something "solid, sensible and suited to the times". Michael Blythe's latest iPartners inFocus looks at the budget which delivered what was promised – some (By Michael Blythe, 26th October 2022)

iPartners inFocus - Budget ‘22 – Once more to the breech!

Budget ‘22 – Once more to the breech!

The Budget delivered what was promised – something "solid, sensible, and suited to the times".

● At one level the Budget defies the gloom that underpinned its formulation.

● Longer-run figuring shows deficits all the way out to 2032/33, with little lasting deficit reduction.

● The flat deficit profile requires an extraordinary degree of expenditure restraint.

● The unexpected lift in inflation rates cuts across much of the Budget figuring and policy proposals.

● Stage 3 tax cuts have been widely criticised – but there are good reasons they should go ahead.

Treasurer Chalmers persistent refrain in the lead up to the October Budget revolved around:

• the “dark storm clouds” that were building offshore;

• rampant inflation that was generating a cost-of-living squeeze, pressuring budget spending and driving a “blunt and brutal” interest rate response;

• the constraints imposed by an inherited $1 trillion of government debt courtesy of “a wasted decade of missed opportunities and warped priorities”; and

• the need to keep the faith and deliver on election promises.

As a result, the Budget needed to be "solid, sensible and suited to the times." And this is essentially what was delivered.

Economic forecasts were downgraded – both domestically and offshore. The central policy focus is on delivering support to household budgets. The $1 trillion debt “target” is still there. The previous government was awarded a fair share of the blame for the apparent economic mess. And a start was made on delivering election commitments.

It is reasonable to ask, however, just how “bad” is it?. GDP growth forecasts were cut and unemployment projections lifted. But they remain a long way from recession-type readings. Inflation rates are close to a peak – they are set to slow sharply from end 2022.

And real wages will grow again. Budget deficits persist but they are lower in aggregate than expected just a few short months ago. It seems we can still afford the Stage 3 tax cuts. The projections may still show gross government debt hitting the $1 trillion mark in 2023/24. But the debt profile out to 2025/26 is improved.

Most of the Budget was (very) well telegraphed in the lead up to Budget night. From that perspective, the main “surprise” was the housing initiatives that were foreshadowed late in the piece. Housing as an asset class looks ripe for development.

The main “disappointment” was the flatlining of Budget deficits at around the 2% of GDP mark all the way out to 2032/33.

The numbers

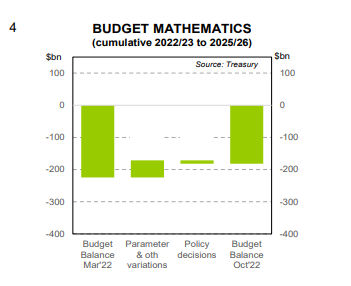

Mini Budgets or Economic Statements are an often-used part of the government’s fiscal repertoire. But having two Budgets in the one fiscal year is new.

There is a seven-month gap between the 2022/23 Budget in March and the 2022/23 October Budget (as it will be known). A staggering amount changed in that relatively short period. If nothing else, that change highlights the need for caution when looking at fiscal calculations.

A quick look at the numbers underlines the point. The expectation in March was that the 2021/22 underlying budget deficit would come in at $79.8 bn. When the actual outcome was announced in September, the deficit printed at $32.0 bn.

We can criticise Treasury’s forecasting ability. But there is no denying the resilience of the Australian fiscal machine. After a COVID-driven departure from “normal” budget outcomes, the return to those pre-COVID norms was remarkably rapid (Chart 3).

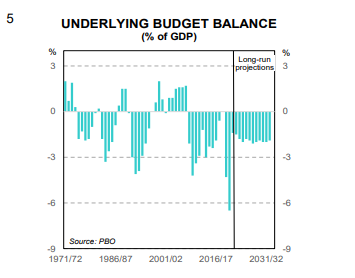

Fast forward to October’s Budget 2.0. The expectation in March was that deficits would cumulate up to $225bn over the four years to 2025/26.

The Budget mathematics (Chart 4) now show that parameter & other variations – or “the economy” – will improve the budget bottom line by $53bn over the period. Some $10.5bn is handed back through policy initiatives. The cumulative budget deficits over the next 4 years now stands at $182bn.

The medium-term fiscal strategy previously centred on the government balancing the budget over the course of the economic cycle. This objective has quietly morphed into allowing the automatic stabilisers to work and restraining spending growth.

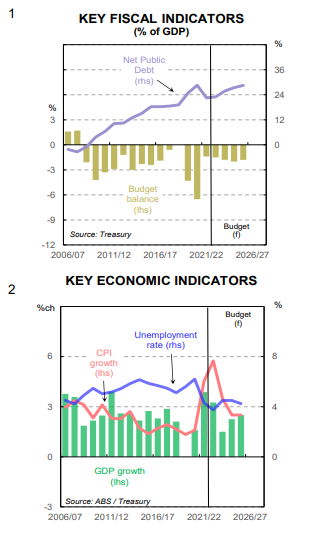

As a result, longer-run budget figuring shows deficits stretch all the way out to 2032/33 (Chart 5). And there is little in the way of lasting deficit reduction achieved. The Budget Report Card, if it existed, would have a “must try harder” stamp.

The flat deficit profile requires an extraordinary amount of expenditure restraint. Real spending growth is limited to 0.3%pa over the next four years (vs 2.2%pa in the pre-pandemic period). This is a stretch target to say the least.

The flat deficit profile means government debt outstanding will fail to meet the medium-term fiscal aim of stabilising and then reducing debt as a share of GDP. Another “must try harder” on that Budget Report Card!

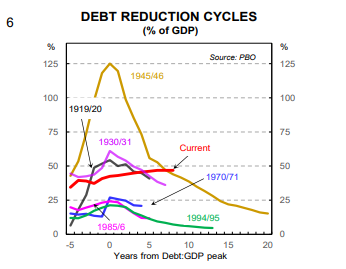

The lack of progress in winding back the debt ratio is disappointing relative to previous debt reduction cycles (Chart 6).

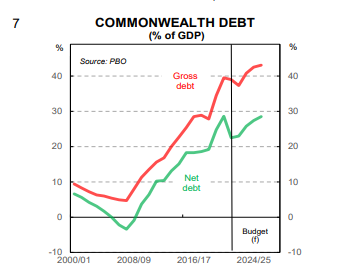

The main points of interest in the debt projections is the growing divergence between net debt and gross debt (Chart 7).

The gross-net divergence reflects the old budget accounting smokescreen whereby some actions are “off budget”. So gross debt rises as the government sets up instrumentalities such as the National Reconstruction Fund and Rewiring the Nation. But net debt is not affected because the debt will be offset by the organisation’s assets.

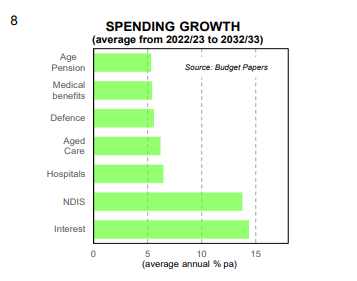

Wherever the debt may reside, it still needs to be serviced and will add to government interest payments. Debt servicing costs are now the fastest growing components of government spending (Chart 8).

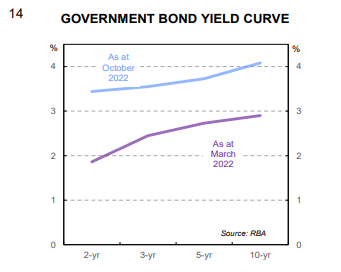

Budget figuring assumes a weighted average bond yield of around 3¾%. Bond yields in the 3-10’s part of the curve are currently in a 3½-4% range.

The credit goes to the Australian Office of Financial Management (AOFM). They manage the national debt for the Government. The AOFM took full advantage of earlier low interest rates to issue more long-term debt. The average duration of Commonwealth government bonds on issue now stands at over 7 years). They have essentially “locked in” low interest rates for an extended period.

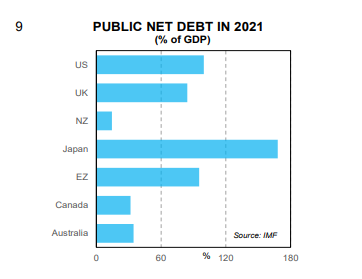

The debt-is-evil mentality that dominated much of the fiscal debate for the past couple of decades was slowly losing steam. The “demonising” of the $1 trillion number brought the debate back into focus. That line in the sand is still there (although it now represents a significantly smaller share of GDP). In any event, Australia’s fiscal balance sheet still looks very good relative to most other countries (Chart 8).

The Budget & inflation

Various aspects of the inflation story are very much in evidence in the October Budget.

The emphasis of the “new” policy is to alleviate some of the cost-of-living pressures on household budgets. Households are caught in a squeeze between falling real wages and rising costs.

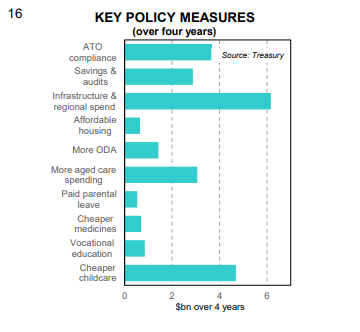

The main measures involve support for childcare, reducing the co-payment under the Pharmaceutical Benefits Scheme, boosting parental leave and some assistance for education costs like Fee-Free TAFE (Chart 16). The Government will also support wage rises for lower income earners.

The measures are all worthwhile. But they probably won’t shift the dial too much. The spending involved of around $7bn equates to ½% of household disposable income (over 4 years). The decision to lift the migration target by 35k to 195k in 2022/23 will boost labour supply and may make wage rises more difficult to achieve.

Policy makers have been quite clever in designing policies that will help slow inflation. The childcare and pharmaceuticals measures, for example, will reduce both payments and the CPI.

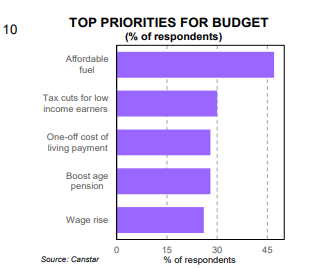

It’s not all a one-way street. Budget forecasts show no real wage growth before 2023/24. And a recent survey by Canstar shows the government failed to deliver the sorts of assistance that households want (Chart 10). Top of the list is affordable fuel. But the temporary fuel excise reduction is now at an end. Households also want cuts to tax rates for low income earners. The government has stuck with the earlier Coalition decision not to extend the low & middle income tax offset (LMITO). Effectively it means a tax rise (via a smaller refund) in 2023/24).

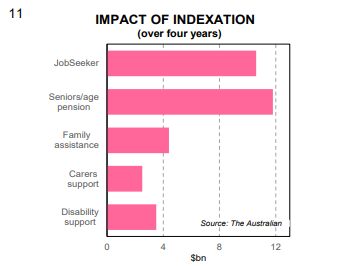

Inflation also feeds back into the Budget. The government highlighted the impact of rising inflation on key areas of spending in the run up to the Budget. The extra spending required by CPI indexation in area like the age pension and JobSeeker payments adds up to more than $30bn over the next four years (Chart 11).

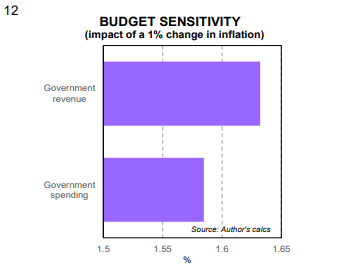

What received less attention was the way higher inflation rates play out across other Budget aggregates.

Many spending programs are indexed to inflation. But some admittedly simple analysis shows that government revenue has the greater leverage to inflation (Chart 12). So higher inflation rates may be a net positive for the Budget bottom line.

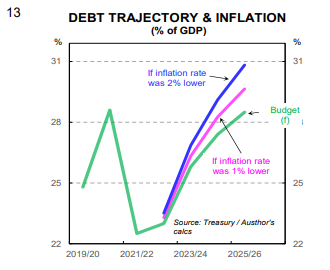

Inflation also lends a hand when it comes to Budget ratios. Higher inflation means nominal GDP grows at a faster pace than otherwise, reducing those ratios to GDP as a result.

The government debt:GDP ratio, for example, could look quite different - all else equal (Chart 13). The official figuring has the net debt GDP ratio at 28.5% in 2025/26. But that ratio would be more than 2ppts higher if inflation rates were 2%ppts lower.

Presentationally, that difference is significant.

Inflation also affects the value of government debt. Higher inflation means higher interest rates across the yield curve (Chart 14). The mechanics of bond pricing means that price of government debt is inversely related to the yield. Higher yields mean lower prices and the value of debt outstanding falls.

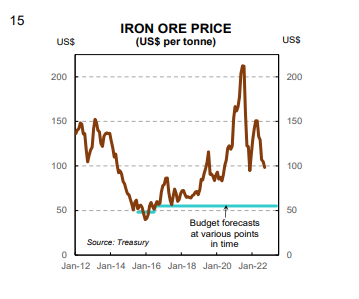

It is not all about inflation. Budget figuring is also built on deflation in commodity prices. The Budget employs what has been the standard assumption in recent years that the iron ore price will eventually subside to US$55 per tonne. By Q1 2023 in this Budget. Economists learn to never change a good forecast – because it will be right eventually. But the iron ore forecast has proved too pessimistic for a very long time (Chart 15). Similar comments apply to other commodity price assumptions.

It is a conservative assumption that does impose some discipline on spending plans. Budget sensitivity analysis shows that a delay in commodity prices dropping to longer run averages by three months would boost nominal GDP by $44bn and tax receipts by $10bn (over the next 3 years).

The benefits of higher commodity prices were typically shared across business (profits), households (wages) and government (revenue). But the flow through to wages since 2016 is problematic.

The lack of flow through explains why faster wages growth is a policy priority. The most effective fiscal tool to this end is getting the tax system right.

Australia’s over reliance on taxing households is a long-running feature of the economic debate.

Other measures

Beyond households, the relatively modest package of measures is built around delivering on the government’s election commitments.

The bulk of the other new spending goes on dealing with the aged care crisis and infrastructure (Chart 16). Savings measures generally revolve around the tired old collection of spending audits and ATO compliance initiatives.

There are a range of other measures that are essentially “off budget”. They involve establishing a range of funds to use lower-cost government funding to meet policy challenges such as climate change. Rewiring the Nation will modernise the electricity grid. Powering the Regions will focus on renewable energy projects. The Driving the Nation Fund will promote electric vehicles. The National Reconstruction Fund will provide capital for priority industries like agriculture, medical science, renewables, defence, transport and so on.

Housing is a focus with the government striking an Housing Accord with investors and industry to build more affordable housing. The rather ambitious target is 1 million new dwellings over the five years from 2024.

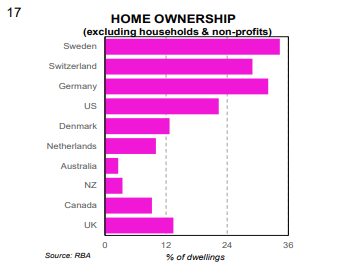

The share of the Australian housing stock held by sectors other than households is small. Corporates and institutions are not big investors in residential real estate. In the US and some European countries, however, this share is well over 20% (Chart 17). Housing as an asset class looks ripe for development.

The elephant in the room relates to the Stage 3 tax cuts. Understandably, a new government is keen to be seen standing by its election promises. But with a Budget under pressure and the appetite to spend as great as ever, the temptation to ditch the cuts is strong. Community support has reportedly waned, although that depends on whether you are in line for a tax cut or not. The Treasurer’s body language suggests he wouldn’t be adverse to swinging the axe. And with the cuts scheduled to take effect only from 2024/25, there is clearly time for a rethink. But should the tax cuts be abandoned?

In defence of Stage 3

The Stage 3 tax cuts involve:

removing the $120-180k tax bracket;

lifting the top tax threshold from $180k to $200k; and

lowering the marginal rate for the $45k-$200k bracket from 32.5% to 30%.

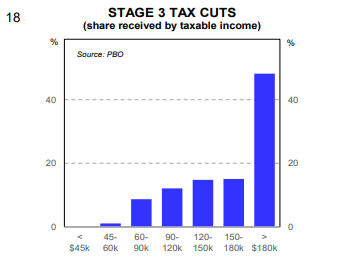

The gold standard for assessing a Budget is “what’s in it for me?”. The perception is that there is no benefit for the average taxpayer. It all goes to the top end of town. But analysis by the Parliamentary Budget Office (PBO) shows that the benefits are spread more widely (Chart 18).

It is true that the upper end of the income range receives a larger share of the benefit. But this analysis is part of the reason why fiscal reform is so difficult. A genuine analysis of Stage 3 needs more than just a focus on the winners and losers. A more holistic approach that looks at all of government is required. There is the benefits side of the tax/spend equation to consider as well.

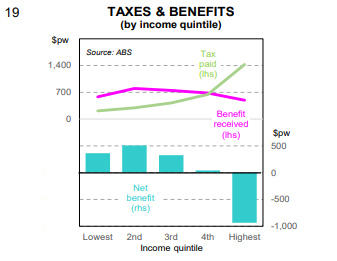

A system-wide look reveals that higher income groups pay more in tax than they receive in benefits (Chart 19). In fact, it is only the top income quintile (the top 20% of income earners) that pay net tax.

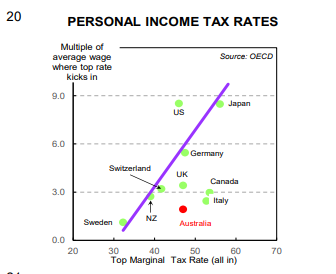

A global comparison shows that Australia’s top marginal tax rate kicks in at an unusually low multiple of average weekly earnings (Chart 20). And that top rate is towards the top end of the global range.

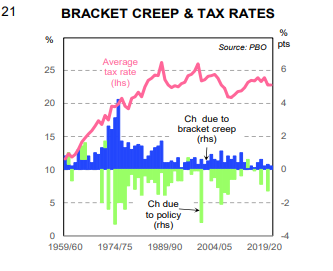

Finally, inflation is important again. Bracket creep, where taxpayers edge up into higher tax brackets as wages rise, is a great way to generate revenue. Even with the subdued wages growth of recent years, bracket creep has acted to push up the average tax rate (blue bars on Chart 21). Bracket creep can only be dealt with by indexing tax brackets. Or cutting tax rates from time to time.

The Budget & the economy

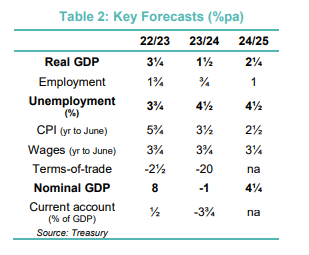

Budget economic forecasts are summarised in Table 2.

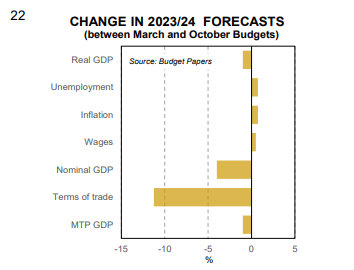

The forecasts stop short of recession. But the current figuring represents a significant downgrade form the economic backdrop envisaged back in March (Chart 22). The global backdrop is particularly problematic.

Economic growth in 2023/24 is slower than previously thought. And unemployment and inflation rates are higher. A bigger fall in the terms of trade means an outright decline in nominal GDP (or the tax base). The downgrade is one of the reasons policy makers only made a limited progress in cutting prospective budget deficits.

As noted, what is left is an economy that skates past recession with only limited damage to the labour market. An unemployment rate peaking at 4½% would still be at the lower end of the range of the past couple of decades. Inflation is expected to return to “normal” and wages return to the “normal” situation where they run ahead of prices.

Even with the downgrades, risks remain to the downside. The word “risk” appears 300 times in Budget paper No 1 (vs 230 in the March Budget papers).

Much needs to go rights to achieve the Budget projections. In particular, the consumer is an essential component of the underlying Budget parameters. The Budget also has business capex playing a major role. But residential investment declines as the earlier boom unwinds. And public spending slows after the rapid growth associated with the pandemic. The external sector plays a neutral role in net terms in the growth profile.

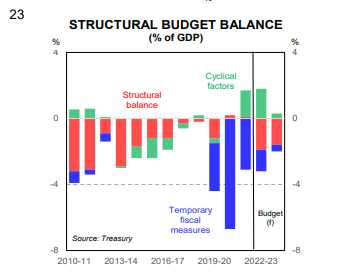

Policy settings contribute to the overall outcome. Monetary policy is moving into restrictive territory. Fiscal settings imply a small contraction as the structural budget deficit narrows. (Chart 23)

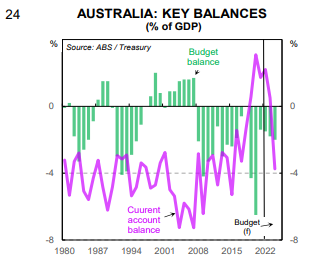

The current account balance is projected to collapse back into deficit. The extraordinary turnaround of nearly 6% of GDP between 2022 and 2024 is the mechanical outcome of an equally impressive collapse in Australia’s terms-of-trade. The forecasts look way too pessimistic.

For the accountants, a surplus means we no longer need to borrow from the rest of the world. Our exposure to global risks is lower as a result. The current account surplus is one reason why the agencies are happy to leave Australia with a AAA credit rating despite ongoing budget deficits (Chart 24). This rating could be at risk if the current account forecasts prove correct.

Meanwhile, those dark storm clouds the Treasurer talks about means I’m off to buy an umbrella!

Disclaimer

This report provides general information and is not intended to be an investment research report. Any views or opinions expressed are solely those of the author. They do not represent financial advice.

This report has been prepared without taking into account your objectives, financial situation, knowledge, experience or needs. It is not to be construed as a solicitation or an offer to buy or sell any securities or financial instruments. Or as a recommendation and/or investment advice. Before acting on the information in this report, you should consider the appropriateness and suitability of the information to your own objectives, financial situation and needs. And, if necessary, seek appropriate professional or financial advice, including tax and legal advice